Target audiences for entrepreneurship education should include both present and future business owners, as well as government personnel

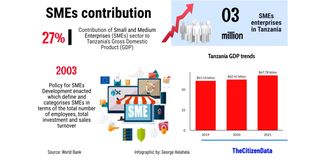

Dar es Salaam. The Small and Medium Enterprise Development Policy of 2003 defines and categorizes SMEs in terms of the total number of employees, total investment and sales turnover.

This is a common way of categorizing MSMEs globally because it enables the government to support, protect and nurture the ‘underdogs’ in the business sector.

But it could lead to babysitting. It could result in the ‘charity mentality’ to stunted businesses that remain micro and small forever, analysts say. Some micro and small and even some medium businesses are established to serve subsistence purposes with neither ambition for growth nor vision for the future.

The issue arises when policy implementers fail to acknowledge this lack of growth and continue to provide the meager “assistance,” believing falsely that certain SMEs could continue to exist as micro and small businesses for however long is necessary. This results in a policy trap.

That is why imparting entrepreneurial skills to a broader section, beyond those who have already established businesses, is so crucial to unleashing the entrepreneurship spirit in the country. Entrepreneurship education should , therefore, target existing entrepreneurs and potential entrepreneurs such as civil servants, salaried workers in the private sector and people living in the margins of the society such as the disabled. For this to happen there is need to scout for individuals who are self-starters and serial entrepreneurs. These should further be trained on entrepreneurship, given the requisite support and launched into business. Tanzania, with its versatile commercial culture, has plenty of potential serial entrepreneurs.

That some Tanzanians, who started out as micro entrepreneurs decades ago, have established business operations in eastern, central and southern African countries testifies to this fact.

Even in North America, Europe, South Korea, Japan and even Brazil there are hundreds of multinationals that started out as micro and small enterprises a century ago. Having spotted their potential the governments set out to ‘boost’ by providing all kind of support and protection.

The nature of startups and the manner in which they mobilize resources have changed since then, especially in digital technology sector. But there are lots of entrepreneurial practices in startups financing that have remained constant in countries like Tanzania with less developed financial and capital markets.

One of the biggest challenges facing Tanzanian entrepreneurs is the startup capital financing. As it turns out, however, many Tanzanians rush to invest in fixed assets that do not generate revenues, instead of using the same investments to launch their small businesses. One of the most common types of passive, fixed assets is residential houses. Most Tanzanians feel compelled to build and live in their own houses. It’s because of peer and societal pressure that has made the word ‘renting’ a dirty word. It is always good to own a house but the lack of affordable housing finance means that many families make untold sacrifices and “break” their backs to just to build and own that house.

The processing of building the house does not generate any revenue for the household. If anything it eats up even the family’s remaining meagre savings. After the construction is completed, the new house, as an asset, does not bring any income.

Many families have entered into dire economic straits soon after moving into their houses because the asset has dried up the household’s savings and is not a cash cow. If it’s a big house that means more utility bills to pay.

And if the family turns into entrepreneurship, then finding startup capital becomes a challenge. The finances spent on building the house could have served as an adequate capital to start and maintain a business.

It is the question of mentality; a poor mentality that can be changed with the right training.

Mohammed Dewji, a business leader, a philanthropist and a scion of a prominent entrepreneurial family, has some three point advice for aspiring, and especially young, Tanzanian entrepreneurs in terms of financing their startups.

“First and foremost, you know, we need to create a culture of saving. If you save slowly slowly slowly over time then you will create some capital and that can help you to do business,” he says in a video clip posted to his LinkedIn page on November 23, 2022.

“Number two. The second mistake that we Tanzanians do. Many a times I speak to so many of my friends, you know they are living in a rented houses, but they want a better house. So now by building a house, as much as building a house is important, but building a business that generates cash-flow [first] and then building a house makes more sense... But they want to go and build a house so that means they fix a capital in the house and there is no return on it. So if I was a Tanzanian young entrepreneur I wouldn’t care, I would live in a rented house but collect that capital and invest in a business,” he adds.

He finishes by saying; “Number three, If you have built a house that means you have a collateral. With a collateral now banks are, you know, giving excess to capital. I suggest as micro-credit agencies..., I think they are very expensive. So if you have collateral then go to commercial bank and get you loan as long as you have done your pre-feasibility of the business that you want to do thoroughly.”