According to the central bank policy, a bank that extends credit to agriculture shall be eligible to a reduction in SMR amount, equivalent to the loan extended

Dar es Salaam. When Covid-19 hit the world, many economic activities were disrupted, making it difficult for banks to lend to the dormant businesses.

The government responded with a set of measures that did not only address the situation of the time but also created a new environment in the banking industry in an attempt to stimulate the financing of economic activities.

Related

Today, the agriculture sector has been one of the financing recipients with fast-growing credit, sending hopes to farmers.

“At least we can access the agriculture loans at an interest rate of nine percent per annum,” said Manyara-based farmer Clemence Sisso.

“You know, agriculture is a bit challenging even if you get the loan at zero percent because there are weather issues.

At least, the decrease in the interest rate is encouraging us to do more,” he added.

Agriculture employs more than 60 percent of the Tanzanian working population but accounts for only 28 percent of the gross domestic product (GDP). The economy is dominated by services at 40 percent, followed by industry and construction at 32 percent.

The sector is the fourth recipient of bank loans after personal loans, trade, and manufacturing.

Agriculture financing is done by the government-owned Tanzania Agricultural Development Bank (TADB), which is a specialised development financial institution, and other commercial banks that have a window for agriculture loans.

The government increased the capital of the TADB from Sh60 billion in 2021 to Sh268 billion in 2022, according to the Agriculture budget speech that was read in Parliament in May 2022.

TADB also guarantees smallholder farmers who borrow from other partner banks, covering 50 percent of the loans.

After the outbreak of Covid-19 which affected the financing of most economic activities last year, the Bank of Tanzania came up with measures that would provide great impetus to the pace of credit to the private sector and lower interest rates.

The measures were also part of attempts to accelerate the recovery of the economy from the effects of the pandemic.

The central bank measures included the reduction of the statutory minimum reserve requirement (SMR)—the amount a bank deposits at the BoT.

According to the central bank policy, a bank that extends credit to agriculture shall be eligible for a reduction in the SMR amount, equivalent to the loan extended.

In addition, a bank shall be required to submit evidence of lending to agriculture at an interest rate not exceeding 10 percent per annum. This measure is intended to increase lending to agriculture, which is the mainstay of most Tanzanians. It also aimed to reduce interest rates on loans to agriculture.

The central bank also introduced a special loan amounting to Sh1 trillion to banks and other financial institutions for on-lending to the private sector. The central bank said would provide the special loan to banks and other financial institutions at three percent per annum for pre-financing or re-financing of new loans to the private sector.

A bank wishing to access the special loan facility should be required to charge an interest rate not exceeding 10 percent per annum on loans extended to the private sector. The measure is intended to increase liquidity for banks and reduce lending rates.

Today, the initiatives are paying off with the increase in credit to the private sector, the reduction of interest rates, and, more importantly, the increase in the speed of lending to the agriculture sector.

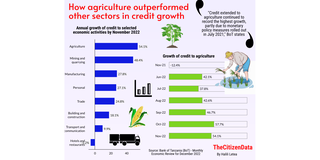

For instance, in the year ending October 2022, private sector credit recorded a year-on-year growth of 23.7 percent, compared to 5.6 percent recorded in October 2021. The target was to record a growth of 10.7 percent for the current (2022/23) financial year.

The performance of private sector credit is attributed to normalisation of economic activity following Covid-19 pandemic, coupled with supportive monetary policy conditions, the BoT said.

On the other hand, the agriculture sector continued to record the highest growth rate, attributable to the monetary policy measures rolled out to support cost-effective credit intermediation in the sector.

The credit to agriculture grew by 57.7 percent during the 12 months to October 2022, compared to a decline of 14 percent during the previous period, according to the central bank data.

“I have managed to almost triple my farming size after securing the loan at an interest rate lower than 10 percent,” said Mr Hassan Omary, another Manyara farmer, adding that such efforts would support food sufficiency in Tanzania.

“I believe more people will get into farming if they have access to such financing. That is good for food security and individual economies,” he added.

Tanzania is estimated to have at least 10 percent of the population living with insufficient food consumption, according to analysis by the ONE Campaign, a global campaign and advocacy organization.

As of December 27, 2022, the organisation estimated that there were 614 million people around the world with insecure food consumption, a -0.4 percent change in the last month.

More financial reforms

Tanzania also undertook other Covid-related reforms in the financial sector, which are now creating a new landscape for the operators.

These reforms include the relaxation of agent banking eligibility criteria. The central bank removed the regulatory requirement of business experience of at least 18 months for applicants of agent banking business.

Instead, applicants for the agent banking business are required to have a National Identity Card or National ID Number.

The policy measure was expected to contribute to an increase in loanable funds for banks through deposit mobilisation. The measure is also intended to lower lending rates.

The central bank also introduced limitations on the interest rate paid on mobile money trust accounts. Mobile money trust account balances held with banks should be eligible for an interest rate not exceeding the rate offered on savings deposit accounts by the respective bank.

The measure was intended to contribute to lowering the cost of funds for banks, thus helping to reduce lending rates.

Another measure is the reduction of the risk weight on loans. The Bank of Tanzania reduced the weight of risk on different categories of loans in the computation of the regulatory capital requirement of banks. This measure would provide an opportunity for banks to extend more credit to the private sector.

This story was produced in partnership with the ONE Campaign, a global campaign and advocacy organisation