Should Tanzania be concerned about its budget deficit?

By Joseph Semboja and Derick Msafiri

Introduction

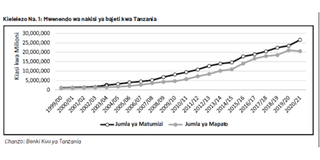

Public spending enables governments to fulfill their objectives and promises to citizens on the provision of public goods and services or the redistribution of resources. This is true for rich and poor countries and, Tanzania is no exception to this. Between 1999/00 and 2020/21, public expenditures rose by 26-fold while the government’s revenue from taxes and non-taxes rose by 20-fold, leading to an increase in the budget deficit by 15-fold (Figure 1).

Sustainability of the Budget Deficit

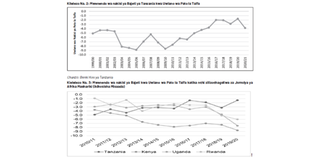

The question is whether this trend of the budget deficit is sustainable. The simple logic of budget deficit sustainability is to relate the deficit with economic growth. Experts differ on the exact size of a sustainable budget deficit, but they generally cite figures of 5% of GDP or less (Afonso and Jalles, 2013; Akosah, 2013). The East African Community (EAC) has adopted a cut-off of 3%. Figure 2 shows that Tanzania consistently moved towards the 3% target since 2005/06, achieved it in 2016/17, and stayed within the target for four years until 2020/21 when it was missed. Figure 3 shows that Tanzania also outperformed other EAC members since 2015/16. Therefore, from this simple indicator, the Tanzanian fiscal deficit has been ‘sustainable’ in recent years.

But the ability of a government to continuously finance its budget deficit depends not only on the growth and size of its budget deficit and the economy but also on the interest rates on money borrowed to finance it and inflation. (Langdana & Murphy, 2014). Interest rates affect the cost of debt services, and inflation reduces the real value of nominal liabilities and thus the real value of the outstanding debt and debt service costs. Following this, and based on the Dornbush Model of Fiscal Deficit Sustainability, the effective (real) cost or burden of the debt service can be expressed as follows:

EBDS as a percent of GDP= (Debt/GDP) x (Real interest rate-GDP growth rate)

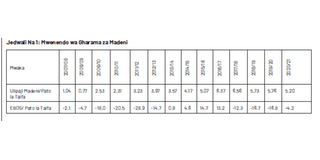

Table 1 shows that the trend of the effective burden of debt service (EBDS) in Tanzania from 2007/08 to 2020/21 has gone through three distinct phases. During the first and third phases, 2007/08 - 2012/13 and 2017/18 - 2020/21, the country’s debt service did not exceed the economy’s ability to continuously fund it. During the two phases, the burden of debt service was financially sustainable. However, the situation was different during the second phase, 2013/14 - 2016/17, when the debt service exceeded the economy’s ability to absorb it through economic growth and inflation. Therefore, in ten out of fourteen years, the country’s debt service burden was financially manageable.

Does the trend of the budget deficit raise policy concerns?

Is it sufficient that the budget deficit is financially manageable? We respond to this question by reviewing the structure and trend of public expenditures and their consequences on fiscal policy space. Figure 4 shows a gradual but consistent policy shift between development and recurrent expenditures, in favour of the former. Between 2002/3 and 2020/21 the share of the recurrent expenditures declined from 81% to 56%, as the development expenditures were favoured with the balance. A government decision made in 2015/16 to fix the share of the development budget at 35-40%, effectively made the development expenditures a binding commitment in the budget.

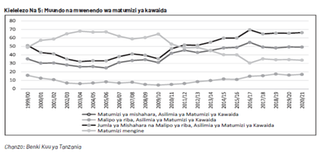

The impact of the policy shift in favour of development expenditures is seen in the structure and trend of the recurrent expenditures presented in Figure 5, showing the share of the ‘other charges’ (OC) declining consistently. This is because wages, salaries, and interest payments are equally binding commitments that must be met. It is also interesting to note that the share of interest payments has been rising faster than the other recurrent expenditure items. Therefore, the share of OC within the recurrent expenditures was halved from 68% in 2003/04 to 34% in 2020/21.

What are the policy implications of the shrinking OC? First, is the limited fiscal policy space or expenditure limitations imposed on the policymakers to exercise discretionary decisions. To the extent that productivity-enhancing expenditures may be compromised. This is made worse by the fact that even within the already constrained OC, provision has been made for protected expenditures, those considered to be too sensitive to cut. 1

The second and most important policy implication is a shrinking operational budget to support the expanding infrastructure. This dilemma of a rapidly expanding capacity amidst a shrinking operational budget is not a new phenomenon in Tanzania. It is a repeat of the 1970s when capacity expansion went hand in hand with high capacity underutilization, resulting in declining productivity in the manufacturing sector. (Wangwe, 1979). Declining OC in public expenditure is reflected in the inadequacy of staff and supplies in health, education, water, and public offices, to mention a few. The result is a seemingly contradictory phenomenon in which public facilities are expanding at the same time as public services are declining.

Concluding Remarks

Two seemingly opposite conclusions arise from the above discussion. First, the fiscal deficit is financially manageable; to a large extent, the country’s budget deficit is financially sustainable and does not pose unnecessary pressure on the economy. Second, the rising burden of debt service, together with the other expenditure priorities has produced a structure of expenditures that leaves very little room for OC as well as discretionary decisions (policy space). The outcome is the poor performance of the expanding public infrastructure, reflected in poor public service provision. This is a policy and developmental concern arising from a constrained budget and must be addressed.

_______________________

1 Out of the already constrained OC, there are other sensitive expenditures that must be funded. They include ration allowances; prisoners’ food; examinations expenses; allowances for foreign service officers; contributions to regional and international organizations; personnel allowances for retired state leaders; subventions to political parties; on-call allowances; and constituency allowance.

REPOA HQ

157 Migombani REPOA streets, Regent Estate, PO Box 33223, Dar es Salaam, Tanzania.