Trend of budget for the development projects within the Ministry of Minerals in the financial years 2020/21 and 2021/22

Background

Budget trends within the Ministry of Minerals (MoM) for the Financial Years (FYs) 2016/2017 to 2019/2020, have been characterised by; inadequate budget allocation and disbursement for development projects; limited public and institutional capacity to enhance transparency and accountability, unstable, constricting and complex policy, legal and institutional frameworks that inhibit effective and efficient implementation of ministerial pri-orities, among others.

It is with the above challenges that HakiRasilimali continues to undertake budget analysis to monitor the budget trends in order to draw lessons to influence reforms towards better budget allocations and disbursements especially for development projects; enhancing dialogue, participation; and capacity building.

For the FY 2021/22, the focus for the analysis has been based on selected ministerial priority areas including enhancing revenue collection and increasing the contribution of the Mining Sector to Gross Domestic Product (GDP); Formalizing and developing the Artisan and SmallScale Miners (ASM) and enabling citizens to participate in the mining sector (Local content), enhancing the capacity of institutions under the Ministry to carry out its responsibilities more effectively, State participation in enhancing the investment environment in the mining sector, Gender discussion in reflective of mining sector related budget, among others.

Extractive sector budget trends: revenue collection, allocation and disbursementNational budget allocations and disbursement:

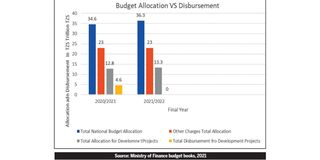

In the FY 2020/2021, the Government of Tanzania (GoT) allocated a total of 12.8 trillion Tanzania Shillings (TZS) (equals to 37% of the total government budget) for development projects across ministries equal. Until January 2021, a total of TZS. 4.7 trillion Equals to 36.7% (i.e. TZS. 3.4 trillion from internal sources and TZS. 1.2 trillion external sources) of the total development budget was disbursed to different Ministries.

The implementation of the 2020/21 National budget in relation to the mining sector reported to implement activities such as the review and amendment of laws, policies and mining agreements; establishment of Twiga Minerals Corporation, Tembo Nickel Corporation’s construction of 39 market centers and 41 mining trading centers; and completion of 4 centers of excellence. In alignment to above, a total of TZS. 13.3 trillion was allocated for development projects (TZS. 10.4 trillion from internal sources and TZS. 2.9 trillion from external sources) in the FY 2021/22.

The allocated budget is meant to implement activities such as enhance the production capacity and service delivery through establishing mining value addition industries (such as the gold smelter in Mwanza), enhance the implementation of the Blueprint for Regulatory Reforms to Improve the Business Environment and development of Mchuchuma-Liganga coal project.

MoM budget allocation and disbursement:

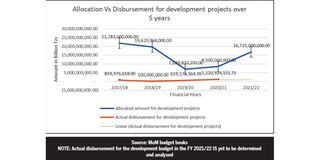

In the FY 2020/21 a total budget of TZS. 62,781,586,000 was approved by the Parliament for MoM whereby a total of TZS. 8,500,000,000 (13.54% of the total budget) was allocated for development projects and TZS. 54,281,586,000 (86.46% of the total budget) was allocated for Other Charges (OC). However, until February 2021, ONLY TZS. 1,220,924,131.73 (only 21.55%) was disbursed to implement activities under the Sustainable Management of Mineral Resources Project (SMMRP).

MoM Budget plans for the FY 2021/22: For the FY 2021/22, MoM plans to use a total of TZS. 68,541,467,000 out of which TZS. 51,816,407,000 (75.6% of the total budget) is proposed for OC, and TZS. 16,725,000,000 (24.40% of the total budget) is planned for development projects related to STAMICO, GST, Mining Commission, the Ministry (i.e. TZS. 15,000,000,000 from Internal sources) and TEITI (i.e. TZS. 1,725,000,000 from external sources).

Findings of the Analysis

HakiRasilimali commends MoM for the work done in the FY 2020/21 and increasing budget allocation for development projects in the FY 2021/22. However, according toHakiRasilimali budget analysis, the trend for revenue collection, allocations and disbursement vis a vis implementation of development projects in the Ministry has been faced with enormous challenges;

a. Insufficient budget allocation for development projects in comparison to amounts allocated for OC. Budget allocation for development projects have always been low in relation to increasing trend of revenue collection for the past five years.

b. Implementation of Projects out of Ministerial Priorities: It has been observed that, devel-opment projects implemented in FY 2020/2021 did not align with ministerial priorities as had been set by MoM.

For instance, under the SMMRP project, MoM reported to implement projects such as road construction, procurement of ICT equipment for security and protection of Mererani and construction of three centres of excellence in Son-gea, Chunya and Mpanda.

This is contrary to planned activities such as construction of the mining core shade for ASM operations, purchase vehicles for research and mineral exploration activities and development of Kiwira Coal project etc. It has been observed that the implemented activities as reported were carried forward from FY 2019/2020.

However, the same is not acknowledged, raising the challenge on accounting for the projects in terms of budget spending in the FY 2020/21.

Recommendations:

1. Support for development projects under MoM need to be strengthened by setting aside strategic and strong financial base to adequately finance development priorities as set by the Ministry.

2. HakiRasilimali urges the Ministry to ensure proper account for activities implemented as carry forward from previous FY to avoid contradictions between actual implemented projects vis a vis the ministerial budget for the specific financial year.

Enhancing revenue collection and mining sector to GDP

The FY 2021/22 budget books show that the growth of the sector by 2019 stood at 17.7%. Further, budget books show the contribution of the sector to GDP growing from 4.8% in 2017 to 5.2% in 2019. However, analysis shows that the contribution of the sector to GDP has remained minimal with an average increase rate of 1% only for almost four years. This is despite the observed increasing revenue and growth rate of the sector.

Challenges:

a) Instability of policy and legal framework to reach 10% contribution to GDP by 2025:

The mining sector has been observed to grow at the rate of 17.7% in comparison to other sectors such as agriculture. This has enhanced total revenue collection made by the government. The Vision 2025 envision a contribution of the sector to reach 10% by the year 2025.

Until 2019, the mining sector contribution to GDP had reached 5.2% despite the observed increase in production and revenue collection in the sector. MoM should ensure that legal, policy and institutional reforms are stable enough to attract new investments (Foreign Direct Investments-FDIs), increase the contribution of the sector to GDP and enhance Tanzanians participation in the mining value chain.

b) The impact of Covid19 in the mining sector:

The outbreak of COVID19 and its impact in the mining sector (such as gold and gemstone production, prices and revenue) in the implementation of 2019/2020, 200/21 FY budget contribution cannot be left undiscussed in the current FY 2021/2022. Globally, the trend of mineral production was significantly impacted by COVID19, whereby Tanzania witnessed a moderate to low mineral production at a rate of 27.3% in late 2019 to 2020. For instance; Government Reports in 2020 show that, gold production (Large scale Mining) was observed to be fluctuating between 2019 to 2020 i.e., gold production was seen to be high in October 2019 at about 1.5 million grams followed by June 2020 at about 1.3 million grams while in June 2019 the production was recorded the lowest at about 447,861.8 grams. Despite the fact that, there were NO restrictions or lockdown measures imposed in Tanzania, the Artisanal and Small Scale Miners (ASM) were strongly impacted by the pandemic caused mainly by global travel restrictions and limited market supply (internationally). This restricted gemstone dealers’ access to export goods to international markets or international buyers from flying into the country.

Recommendations:

1. The Five-Year Development Plan III (FYDP III 2021-2025) should ensure effective implementation of the vision set by the Tanzania Mineral Policy of 2009 in enhancing the contribution of the sector to reach 10% by 2025. FYDP III should also accommodate current growth trends, level of investments injected, on-going negotiations, change of policy, practices and legal regimes, among others. Local development and budget allocations: policy perspectives and options to be considered in the implementation of local content policies and practices in the extractive sector in Tanzania

The concept of Local Content and participation of Tanzanians in Strategic and Investment Projects has been a crucial part of the implementation of the National Economic Empowerment Policy of 2004 which aims to achieve the Government’s goal of building an industrialized economy towards a middle-income economy by 2025.

Ministerial budgets and National Economic Empowerment Council Reports from 2016/17 to 2020/21 show that, local content in Tanzania, has gradually gained momentum among government bodies, companies, and civil society organizations. The fact that, budget reports in the Financial Year 2020/21 are silent on the state of implementation of local content (LC), the FY 2021/22, MoM plans to enforce Large Scale Mining companies to comply with local content provisions on employment, procurement of good and services in Tanzania. However, the implementation of local content initiatives continues to be characterized by the following challenges;

Understanding of Local Content Context in the mining sector:

Tanzania still lacks an integrated nationalized strategy on local content (LC) that cuts across different sectors of economy. As a result, each sector has integrated the understanding of LC as provided by its sectoral instruments. For instance, the Mining (Local content) regulation, 2018 as amended defines Local Content (LC) as the percentage of locally produced materials, personnel, financing, goods and services rendered in the mining industry value chain and which can be measured in monetary terms .

This definition has failed to explicitly define who locals are in LC as a result it has created unrealistic expectations for Tanzanian participation in the sector.

4.2 Enabling regulations for the National Economic Empowerment Act:

Tanzania enacted the National Economic Empowerment Act in 2004, for the purpose of establishing the National Economic Empowerment Council (NEEC), National Economic Empowerment Fund and providing opportunity for Tanzanian to participate in economic activities, however, over 17 years now, there are no enabling regulations to ensure effective and efficient implementation of the Act in realization of Local content Vision in Tanzania.

4.3 Employment:

According to reports (MoM, NEEC, TEITI), employment of locals in the mining sector stands at 7,967 locals and 158 foreigners as reported in theFYs between 2019/2020 to 2020. In FY 2018/2019 reports show employment to stand at 6,623 Tanzanians and 140 foreigners. However, these reports are silent on a quantifiable number of beneficiaries (nationals/locals) employed in the form of direct, indirect and induced employment, and without breakdown on the type of skilled, semi-skilled and unskilled persons.

4.4 Procurement of Goods and services:

Reports from the FY 2020/21 and 2021/22 do not reveal the categorization of goods and services that have been/intended to be locally procured in the mining sector. It should be noted that, Local procurement is a crucial catalyst in the stimulation of upstream linkages and an avenue by which to enhance minerals based industrialization agenda as earmarked in Vision 2025. Procurement starts from the initial resource assessments to mine closure, it includes among others, procurement of services such as financial, legal, and catering; capital goods and construction; consumable materials and replacement parts; bulk services and infrastructure and non-core goods such as boots, uniform etc.

However, procurement of goods and services in the extractive sector has continued to face challenges such as inadequate capacity to enable SMEs to invest, poor standard of goods and services procured locally, inadequate information / research on the capacity of Tanzania to produce goods and services needed by the Mining companiesSecondly, there is no integrated local content supplier’s database as means of increasing visibility in the mineral value chain.

Recommendation:

1. There is need to redefine LC in the context of DOMESTIC capacity to feed into different economic sectors such as extractive, in respect to workforce development, procurement of goods and services. This can be possible only if the Mining Commission and NEEC invest into research / baseline survey to determine the quality and quantity of goods and services that a country will be able to feed into the extractive sector value chain.

The result of the survey should be able to set a precedent for a Domestic Content of the agreed standards of employment, good and services that Tanzanians will be able to feed into the sector

2. Empowerment is a main component in the framework of achieving local content implementation. HakiRasilimali is therefore, recommending for a review of the National Empowerment Act and Policy to be the main legislation on local content in Tanzania for the purpose of having an integrated legislation across sectors of the economy.

3. The National Economic Empowerment Council (NEEC) should be reformed to an Authority or Commission in order to give it more mandates. The current structure empowers NEEC to play an advisory role in driving the Local Content agenda in Tanzania.

4. In order to realize a mineral basedindustrialization state, Tanzania needs to strengthen the environment for its backward linkage developments. This requires promoting the growth and capacity development of its institutions such as Universities, colleges, vocational training centres, Private sectors, NEEC etc that help to build the socioeconomic assets and infrastructure on which industries depend

5. Establish an online portal for local suppliers that will reduce bureaucracy of registrations and give flexibility to address local capacities. The portal will also provide linkages to local suppliers to harness available opportunities with the mining sector. At the same time, to facilitate the establishment and operationalizing of Enterprise Development centres for the purpose of acquiring locals to access international certification and standards.

4.5 Listing of shares at the Dar es Salaam Stock Exchange (DSE)

In the FYs 2020/21 and 2021/21, reports from MoM are silent on reporting the state of mining companies listing their shares at the DSE. As a means of increasing local participation and take stake in the venture, section 126 of the Mining Act 2010 (CAP 123 Revised Edition 2019) provides for mining companies in Tanzania to list their shares at DSE as per the Capital Market and Securities Act (Section 109).

However, the Mining (Minimum Shareholding and public offering) regulations of 2016 as amended in 2020 (regulation 4 and 5) provide exemption for holders of Special mining Licence (SML) not to list their shares to DSE for agreement reached in relation to non dilutable free carried interest and economic benefit sharing (such as the Government with Barrick Cooperation and Kabanga Nickel in establishing TWIGA and TEMBO).

HakiRasilimali understands that the government is likely to adopt the Barrick-GoT framework agreement for future mining operations. As a result, main major mining operations will not enlist their shares to DSE and thus impact the participation of Tanzanians in mining operations.

Recommendations:

1. There is a need to review the Mining (Minimum Shareholding and public offering) regulations of 2016 as amended in 2020 (regulation 4 and 5) to examine whether it serves the spirit of enactment of section 126 of the Mining Act 2010 (CAP 123 Revised Edition 2019) which aimed at ensuring participation of Tanzanians in the mining sector through purchasing of shares enlisted in DSE.2.

The government should create enabling environment for Tanzanians to participate in the mining sector through acquisition of share enlisted in DSE. This should go hand in hand with capacity enhancement of Tanzanians.

3. Enhancing institutional capacity under MoM to ensure efficient and effective implementation of development projects

In order to ensure effective and efficient implementation of development projects, MoM in the FY 2020/21 and 2021/22 has reported to prioritize the need to enhance capacity of its institutions such as the Tanzania Extractive Industry Transparency Initiative (TEITI) and the State Mining Corporation (STAMICO), among others.

5.1 The Tanzania Extractive Industry Transparency Initiative (TEITI):

a) Inadequate Funding to support development initiatives towards enhancing transparency and accountability:

TEITI has not received fund for development projects since FY 2018/19 to 2020/21. As a result, TEITI has failed and /or delayed completion and publication of reconciled revenue reports. In the FY 2020/21, reports show that some of the TEITI projects were run using the Mining Commission’s disbursed budget, creating ambiguity and con-fusion during budget scrutiny.However, in the FY 2021/22, MoM reports to allocate TZS. 1,725,000,000.00 for TEITI to implement development projects. HakiRasilimali understands that the allocated fund is from external sources, as support from the World Bank under its project Extractive Global Programmatic Support (EGPS).

The grant is expected to implement activities such as facilitating the implementation of EITI standards and capacity building of stakeholders, to facilitate dialogues between the Government and the private sector on impact of the extractive sector in the country and to establish an electronic system to be used by companies and government institutions on reporting payments made by companies to the government.

This is a commendable move to enable TEITI undertake its development projects, specifically complete and publish reconciled reports on payments made by companies to the government.

b) Revenue disclosure and reconciliation exercises by TEITI:

To date, 10 TEITI revenue reconciled reports on payments made by extractive companies Vs receipts by the government from 2009 to 2019. The reports show a discrep-ancy of over TZS. 90 billion and USD 328,865. Special audits have been conducted by the Controller and Auditor General (CAG) on the highest recorded discrepancies realized in the 7th and 8th reports. However, Nonetheless, audited reports by CAG have not been disclosed to further public engagement as it is done with the reconciled reports; Nor has the audited reports been subjected to the discussions in the Parliament.

c) Incompatibility of laws which prohibit CAG role in exercising scrutiny in extractive investment with government interest:

Because of the nature of Mineral Development Agreements (MDAs) and Production Sharing Agreements (PSAs) entered, CAG role within the sector is seen as a third party denying the CAG the opportunity to audit revenues from the sector.

The presence of the CAG is only realised upon request by TEITI to undertake special audit to a realised high materiality threshold of 1% and above. This is contrary to Article 143 of the URT and section 5 and 15 of the Public Audit Act in 2008, on CAG mandate in access to information.

d) Slow progress towards contracts and beneficial ownership disclosure:

Budget books since 2016/17 to date provide no update on the state of disclosure or establishment of registers for contracts and beneficial owners (BO). This is contrary to the Government reaffirmation to disclose contracts and beneficial owners (BO) by year 2021 and adhering to compliance as guided by TEITA legislation and global EITI standards.

Recommendation.

1. MoM should ensure adequate allocation is set for TEIT to enhance Transparency and Accountability as they assist in curbing illicit operations within the extractive sector.

2. A mechanism to ensure discrepancies below or above materiality threshold are resolved, as any loss of revenues from the sector could greatly impact the country’s vision towards economic development and supporting projects that are meant to result into improved wellbeing of Tanzanians.

3. There is a need to amend the TEITA Act to mandate the tabling of TEITI reports before the Parliament for further scrutiny.

4. Amendment of TEITA Act to reform TEITI to an independent institution to ensure efficiency and effectiveness towards enhancing Transparency and accountability as an

Ombudsman institution. This will also enable TEITI to fundraise beyond allocated budget and make independent decisions without the interference MoM.

5.2 The State Mining Corporation (STAMICO)

For the FY 2020/2021, MoM did not account on the exact amount of budget that was disbursed to STAMICO out of TZS. 1,220,924,131.73 received by MoM for its development projects. Whereas, in the FY 2021/22, TZS. 3,020,000,000 (20.13%) out of TZS. 15,000,000 (Internal sources) has been allocated to STAMICO for development projects.

HakiRasilimali COMMENDS Ministerial efforts to strengthening STAMICO, however, findings from the 2019/2020 CAG report shows that STAMICO has continued to operate under loss (with outstanding debt of TZS. 82,352.00 million with capital amounting TZS. 11,947.00 million) that is contributed by underperformance of its subsidiary company STAMIGOLD. HakiRasilimali analysis has observed that STAMICO underperformance has been caused by among others, lack of financial and technical capital, failure to generate own sources making STAMICO dependent, using of Petrol (amounting more than TZS. 7 billion) to generate power to run its operation, catalyzing STAMICO losses as reported.

Recommendations

1. In 2020 STAMICO was reported to pay dividends of TZs 1.1 bill. HakiRasilimali understands that payment of dividend is the requirement of law. However, HakiRasilimali recommend that the Treasury could set a percentage of the dividend to boost STAMICO financial base and costs.

2. STAMICO as a holding company:

MoM should ensure STAMICO undergoes legal and institutional reforms to transform it to a holding company to enable it undertake and manage government shares as per the new Mining Framework agreements and arrangements.

This will as well help STAMICO increases the capacity to boost its capital base by entering into strategic investment partnerships and if possible, acquire loans and invite individual stakeholders who are keen on investing in the company’s’ priorities.

3. Role of CAG to audit companies with GoT stake: transforming STAMICO into a Holding company to undertake and manage government shares as per the new Mining Framework agreements and arrangements, will enable the CAG to audit extractive related companies and satisfy himself of the conduct of such firms, taking an example of the role played by TPDC in the Oil and Gas ventures in Tanzania.

4. Formalizations of the artisan and smallscale mining

Over the years, the ASM sector has continued to grow and its contribution towards revenues has constantly been reported by the government. This is a commendable effort by the government to ensure that strong initiatives such as tax incentives, establishment of markets centers and controls are put in place to ensure full realization of the mining sub sector.

Analysis reports observe that, challenges relating to lack of a Nationalized Mining Vision to support TDV 2025 with subsequent Policies to govern the formalization of the ASM sector; lack of license security superseding large investments, small scale miners’ capacity on record keeping; limited access to credits, finance and inappropriate technology; inadequate research and geological data; multiple taxes with royalty being charged at each stage in the value chain continue; inadequate access to market information to lock smallscale miners into a cycle of subsistence operations with significant negative consequences on the environment and livelihood.

Recommendations:

1. Policy and Legislation:

Developing policy, legal and regulatory provisions along with institutional capacity that integrate ASM into wide rural development strategies and programs. This should take into account of available alternative economic options by involving all stakeholders including relevant government institutions (Ministry of Minerals, Ministry of Land, Agriculture, Local Government Authorities and Revenue Authorities.

2. Training and Capacity Building:

Training and capacity building should be a prerequisite for granting primary mining license (PML). Moreover, training programs and sitebased demonstration centers through Vocation Training Centre etc., aimed at training artisans that can service the ASM subsector and smallscale miners is critical to address challenges such as market information, value addition, record keeping and technology, among others. Also, training ASM community in modern mining and processing methods to reduce environmental damage and degradation and promote environmental assessment or remediation programs. This will help manage collateral negative impacts on other sectors, such as agriculture, land, forestry and livestock.

3. Establishment of an ASM Support Fund (ASF):

HakiRasilimali recommends MoM to establish ASM support fund to support the subsector. MoM could opt to retain a certain percentage of revenue from mineral market centers and mining trading centres to establish the fund, which could support initiatives such as capacity building and enhancement, research and/or exploration exercises.

4. Research and Geological Information:

Capital injection to STAMICO and GST is needed to ensure adequate research and geological information is made available for the ASM sub sector. This information is critical for the smallscale miners to be able to use as collateral to access credits and finances from bankers. It is also recommended that MoM should work with the private sector (through PPP) to fund research and provision of geological information.

MoM should be firm in the enforcement of provisions related to tax incentives provided to ASM but also ensure mechanism are in place to curb illegal mineral trade which denies the government and miners income double taxation practices especially in ruby mining

5. Monitoring and investigations of mining operations (OSHA, environmental and climate, change analysis)

For the FY 2020/2021, MoM reports to conduct Safety, Occupational Health and Environmental Care inspections to mining companies that have identified improvements on the shortcomings identified in previous inspections.

Challenges such as lack regulations to guide for rehabilitation bonds; inadequate review mechanisms for mining closure plans; lack of waste disposal procedures still persist.Secondly, use of mercury has continued to be a major challenge within the ASM sector and limited interventions are in place to address the same. Studies show that, mercury‐dependent artisanal and small‐scale gold mining (ASGM) is the largest source of mercury pollution.

For some time now, communities near these mines have been affected due to mercury contamination of water and soil and subsequent accumulation in food staples, such as fish.

The risks would even be worse to children that could have both physical and mental disabilities. To date, projects to eliminate mercury in gold processing have been predominantly unsuccessful mainly due to the lack of continuity and misplaced objectives and lack of trainings among the ASM sites.

Challenges

1. It has been observed that, companies such as Buzwagi Gold Mining Company is expected to close by June 2021. However, until now observation shows, that no review of the Mining Closure plan and its rehabilitation bond has been reassessed by National Mining Closure Committee to determine the actual costs for the damaged caused.

2. Lack of waste disposal procedure and approved storage dams for North Mara Gold Mining on poisonous mud is still a huge environmental challenge.

Recommendations

1. Review of the Mining Closure plans and its rehabilitation bonds for Mining Companies is critical to be done by the relevant committee.

2. MoM through STAMICO should invest to research for alternative use of Mercury for ASM related operations.

3. While investing into coal mining, the government can also invest more on environmentally friendly energy sources.

4. Fines imposed for environmental pollution should be utilised for rehabilitation of the pollution made as per the “polluter should pay principle.”

Issues to ponder 6. State participation in enhancing the investment environment in the mining sector

Analysis from MoM budget books (2016/17; 2018/19;2019/20; 2020/21 and 2021/22) is showing the government commitment to continue enhancing enabling and conductive investment environment without affecting the prosperity and aspi-rations of the country as a result of such investment, among others.

This is expected to be done by conducting strategic mining research, industrial mining and metallic mining. However, studies by HakiRasilimali on the same, show that, the government could, however, benefit from additional reforms in order to ensure more stability, transparency, and prediction. For instance; the current fiscal regime, policy and legal reforms have been seen to be complex inhibiting the increase of FDI in the sector as there are no new investments that have been realized since the amendment of extractive related laws in 2016 to date.

8.1 New direction for mining agreements VS investments TWIGA, TEMBO and Helium One etc:

We commend the government efforts to ensure the acquisition of 16% of free carried interest, 50/50 share of economic benefits that was hailed as a game-changer in the negotiations with Barrick Gold and using the result of the framework as benchmark to negotiate with other investments.

However, there is a lot that stakeholders in sector still don’t know about the exact and full details of the 1) the GoTBarrick 2020 ‘final’ Framework Agreement, TEMBO Nickel etc. Lack of information and disclosure in such movements continue to contradict section 16 of the TEITA Act of 2015 , nor has there been any oversight role by the Parliament as guided by ection 12 of the Natural Wealth and Resources (Permanent Sovereignty) Act 2017 and Section 4 the Natural Wealth and Resources Contracts (Review and Renegotiation of the Unconscionable terms) Act, 2017 These new negotiations have caused a lot of secrecy thus denying the opportunity for public scrutiny through the Parliament.

8.2 State participation in the Helium gas projects: Dialogue on state participation in the development of Helium Gas projects in Tanzania through Gogo-ta (TZ) Limited and Stahamili (TZ) of discovered Recoverable Helium Resource (2U/P50) of 138Bcf Ruk-wa Region, is limited. For instance, on 22nd March 2021 Helium One Global Limited announced11 the appointment of Mitchell Drilling Limited as drilling contractor for its three well exploration programme expanding exploration programme with the 4th hole, which would also be payable as equity to Mitchell Drilling on its Rukwa Project (100%) in Tanzania.

Notably:

a) To ensure accountability as guided by the law, any transfer of shares needs to be subjected to government approval, control and attracting taxes thereof. Secondly, the press release, lacks details of the project value to determine the share equivalent. To curb Transfer Pricing and other inflations, it is a concern to understand the percentage value of the whole project and cost auditing of the project is vital before such transactions between Helium One and Mitchell Drilling are completed.

b) Being a rare element, the mode of production for helium gas is contrary to how tradition minerals are extracted. Therefore, the current Mining Act and its Fiscal regime does not accommodate the anticipated share to be accrued from the Helium extraction in regards to issues such as royalty charges among others. It is important for the government to take into consideration a regime that would create higher returns from helium production.

7. Gender discussion in reflective of mining sector related budget

Generally, revenue collection, expenditure control and account-ability are guided by The Public Finance Act, of 2001 requiring all revenues (including those of raised from extractives) to be deposited into the Consolidated Fund (CF) which then can be drawn and allocated into various budget votes by the Ministry of Finance as guided by the Appropriation Act, 2019. Once mining related funds are put into the CF, they tend to lose their identity and it can be challenging to track the extent of distribution across different social groups.

Most of these funds (CF) are allocated into big projects such as infrastructure and energy with the 2020/2021 budget setting a priority area on rehabilitation of infrastructure; flagship projects; social services; agriculture and industry.

However, it is worth noting that allocation of fund intended to improve agriculture and health system will have tremendous impact on women. According to the National Bureau of Statistics, agriculture employ almost 4.7 million Tanzanians from whom about 54% are women.

The health sector reform is also important as it has been negatively affecting women’s access to quality health care (eg. Afya ya Uzazi health). However, the sectoral ministries set higher costs for running institutions (as other charges) with inadequate data on specific projects meant for groups such as women, youth and people with disability.

Secondly, representation and legitimacy of women in decision making avenues such as Mining Commission needs to have affirmative decision by Mom. At the moment, membership to the Commission is by virtue of one’s office which may affect gender balance that Vision 2025 intends to cure.

Therefore, amendments of the Mining Act are required to accommodate gender issues in representation, decision making and participation. Recommendation: Gender was not a priority in MoM reports in FY 2020/2021 and 2021/2022.

HakiRasilimali recommends MoM to address gender issues in the mining sector in a number of perspectives including; environmental pollution and its impact; institutional representation; revenue allocation; mining related projects; ASM and local content.