Policy Forum’s Tax Justice Working Group Position Statement on the 2021/2022 National Budget

Preamble

We, the members of the Tax Justice Working Group (TJWG), an initiative of 13 member organizations within Policy Forum (PF) advocating for fairness in taxation;

Having met virtually and physically since the release of the 2021/22 budget statement by the Minister of Finance and Planning in March 2021, and having consulted a number of relevant policy documents and reports on Domestic Resource Mobilization (DRM) and Public Resources Management in relation to the National budget 2021/22 are;

Grateful of the consistent emphasis by Her Excellency Mama Samia Suluhu Hassan, The President of the United Republic of Tanzania on tax justice and fair taxation of all entities; both local and foreign Investors in an effort to maximize domestic revenues while reducing reliance on foreign aid;

Appreciating the good intent and obvious efforts by the Tanzanian Government in clamping down enormous forms of actions and behaviours that cause revenue leakages while widening the tax base, tackling corruption, modernising revenue collection methods to enhance timely revenue collection;

Concerned about the shocking news on the revenue loss and expenditure mismanagement by various public entities as reflected in the 2019/20 Controller and Auditor General’s (CAG) report while the Minister of Finance and Planning is determined to once again raise domestic revenues from TZS 24.1 Trillion in 2020/21 to 26 TZS trillion in 2021/22;

Cognizant of the obvious fact that Effective Public Resources Management is essential for the realization of public goods and reliable social services as well as basic infrastructure for national development;

Solemnly aware of the irrefutable fact that transparency, accountability, People’s participation, Rule of Law and Democracy which are an integral part of the Principles of Good Governance must be observed to avoid revenue loss and maintain standard public services and proper management of public resources;

Therefore, wehereby present our position statement providing our views on the current situation on revenue collection and associated leakages, governance gaps, Government efforts and finally suggested policy and associated recommendations on how Good Governance can maximize DRM, sustainable and efficient utilization of public resources while curbing revenue leakages and misuse of public resources.

Revenue Collection & Expenditure

2.1: Revenue Collection

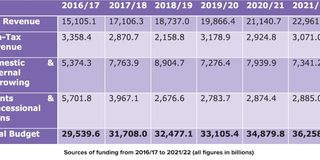

The national budget for the year 2021/22 has seen an increase of 4% rising to TZS. 36.3 trillion from TZS. 34.9 trillion in 2020/21. This is according to the proposal released on 11th March 2021 by the Minister of Finance and Planning while highlighting the National Plan and Budget ceilings for the financial year 2021/2022. Of the TZS. 36.3 trillion to be mobilized, about 72% of the resources are expected to be collected domestically including both tax and non-tax revenue and revenues from the Local Government Authorities.

While all other sources of funds towards financing the National Budget have been inconsistent from 2016/17 to 2020/21, tax revenue has remained the only source that has seen consistent growth every year. For example, tax revenue rose from TZS. 15.1 trillion in 2016/17 to TZS. 19.9 trillion in 2019/20, which is an increase of 24%. The Tanzania Revenue Authority has made significant progress in revenue collection from collecting an average of TZS. 850 billion in 2015/16 per month to TZS. 1.3 trillion in 2019/20 per month.

Overall, there has been steady progress in revenue mobilisation. During the financial year 2019/20 for example, the Government had planned to collect TZS. 33,105.4 billion. At the end of the year, the Government was able to collect TZS. 31,519.5 billion which is 95% of the target.

Despite the observed improvement in revenue generation, reports by the CAG manifest serious mismanagement of public funds by public institutions. For example, the 2020 audit report indicates that seven (7) entities had conducted between 9 and 13 Board meetings during the financial year 2019/20 contrary to Circular No. 12, 2015 of the Treasury Registrar. For instance, TASAC conducted 13 board meetings, TPB Bank, National Housing Corporation (NHC) and Tanzania Communications Regulatory Authority (TCRA) conducted 11 board meetings. A similar Incident is observed when in 2017/18 the Ngorongoro Conservation Area Authority spent TZS 1.10 billion to conduct 20 Board meetings and 6 seminars.

To make matters worse, the report by the CAG covering the year 2019/20 portrays low level of implementation of audit recommendations by the CAG and instructions by the Public Accounts Committee (PAC). Off the 5,483 recommendations given by the CAG for the previous years, the 2019/20 report indicates that only 1,508 (27%) were adequately addressed.

Likewise, PAC being the highest oversight body ought to have been taken seriously when providing instructions to public institutions. However, for the year ending June 2020, the committee had provided a total of 259 instructions to government institutions and only 50% had been adequately addressed.

This calls for deliberate interventions by responsible oversight institutions to ensure the implementation of the recommendations. Oversight institutions should be reminded of the mandate they hold to supervise the duty bearers on behalf of the right holders who are the citizens. Thus have the duty to protect the public funds and combat its misuse as they are a result of the hard work carried out by the citizens aspiring to see that they are effectively managed for the sustainable development of the Nation.

2.2: Revenue Expenditure

Revenue expenditure is key in implementing peoples’ priorities as expressed by the Government and Members of Parliament during the budget debate in the National Assembly. The expenditure is expected to be done by following accountability principles and adherence to the National Budget as passed by the Parliament.

For better scrutiny of revenue expenditure, the CAG’s Report is key to providing insights on Government Expenditures. This is statutorily stipulated in Article 143 of the Constitution of the United Republic of Tanzania and further elaborated by section 10 (1) of the Public Audit Act No. 11 of 2008. section 26 to 29 of the Public Audit Act No. 11 of 2008.

We have noted with great caution a number of concerns regarding the revenue expenditure by public institutions which if not well combated will cause adverse effects in the Domestic Resource Mobilisation, an agendum that has been pioneered by the group for a number of years. A few are highlighted below:

Increased number of LGAs with qualified opinion from 9 in 2018/19 to 53 in 2019/2020 as well as the increase of adverse opinion from zero in 2018/19 to 8 in 2019/20. This shows that there is a deterioration of proper usage of public money which will undoubtedly lessen public confidence hence affecting tax collection.

We have further noted that there have been expenditures in public corporations and Government agencies that seem to be done without conducting proper assessment of costs and benefits. For instance, Tanzania Government Flight Agency (TGFA) spent TZS 3.9 billion on repairing an aircraft that has so far failed to operate. Similarly, over the past five years the Prevention and Combating of Corruption Bureau (PCCB) has opened 2,256 cases of which only 1,926 have been decided. Amongst the decided cases the Government has won 1,013 cases while losing 913 nearly half of all cases which leads us to question the cost to benefit ratio. It is thus advised that PCCB does more groundwork to proceed with cases that carry substantial evidence, this will lighten the load on the judiciary and prisons system.

Another key issue in Government Expenditure is the lack of proper corporate governance check-ups in public and Government Agencies. This leaves a loophole for inappropriate use of funds as there is no internal oversight. For instance, 30 public corporations lack Board of Directors while 11 corporations did not submit expenditure files for auditing. This is a very serious concern to public funds accountability.

On another note, revenue issued as loans to Women, Youth and Persons with Disabilities is not recovered accordingly. For instance, 130 Local Government Authorities (LGAs) issued loans amounting to TZS 42.9 billion. Unfortunately, 65% of the loans were not recovered amounting to TZS 27.8 billion. This will eventually decrease the opportunity for more people to access loans.

There are also incidents of non-expenditure of funds given to local governments. For instance, in 2019/20 TZS 10.6 billion from 26 LGAs were not used to implement 55 development projects. Similarly, 40 LGAs in year 2019/20 completed more than 68 development projects in health, water, education and agriculture as well as other sectors. All these amounted to TZS 18.3 billion. Unfortunately, the projects were not in use. For instance, the Bukoba District Hospital cost amounts to TZS 1.80 billion. This denies the provision of intended social services to citizens in need. Thus, there is a need for the Government to question the LGAs as to why they fail to execute their projects on time.

In the year 2019/20, the Government managed to collect 95% of the approved budget but there was an under-release of 46% of approved budgets to development projects. This under-release is not in proportion with the amount collected.

A significant portion of Government expenditure is used in procurement of different goods and services. The procurement for these is governed by laws and regulations. However, in 2019/20 the CAG’s report showed red flags of corruption and fraud in procurement and contract management amounting to TZS 1,377.87 billion. Procurement procedures were not adhered to, thus creating an environment of fraud and corruption in the public procurement process.

Efforts in Public Resource Management

The financial year 2020/2021 has been unlike any other. With the world reeling from a global pandemic that has struck developed and developing nations alike, there has been a need for new and innovative ways to mobilize resources to meet the needs of the nation as well as to curb the effects brought about by the pandemic. The Tanzanian government has, for the past year, made various efforts to collect revenue and increase sources of income to meet its ever-changing needs. Furthermore, the government has placed efforts in the extractives industry in a bid to realize the benefits of mineral resources.

During his speech to the Parliament on national development and budget for the year 2021/2022, the Minister for Finance & Planning by then, Dr. Philip Mpango, highlighted Tanzania’s economic growth putting more emphasis on domestic resource mobilization and the management of the resources realized. This is important as over the past five years the government of the late Dr. John Pombe Magufuli made great effort to modernize infrastructure and this can be seen through the expansion of the nation’s transport infrastructure. The financial year 2020/21 was not exceptional, 37% of the budget was dedicated towards development projects including mega projects such as the standard gauge railway, the Julius Nyerere hydro power plant, airport installations and aircraft purchase.

According to the Prime Ministers speech, the multitude of projects as well as funds to operate the government were sourced from various areas, with the government having collected 17.1 trillion Tanzanian shillings from both foreign and domestic sources. Of these, 87.9% was collected from domestic sources such as the Tanzania Revenue Authority (TRA) as well as LGAs. Revenue collection, as a part of domestic resource mobilization, was mentioned to have increased remarkably and as a result internal sources of revenue have accounted for the bulk of government expenditure.

The extractive sector has also burgeoned as a source of revenue. The extractive sector has grown over 50% in the past two years, with the Government collecting TZS 307.3 billion worth of revenue from the extractive sector (July 2020/January 2021) as compared to TZS 194 billion collected in the year 2016/2017. Tremendous progress has been made pertaining to public resource management although much is yet to be done.

Recommendations

4.1 We urge Tanzanian policy makers to once again influence mobilization of domestic revenue and make sure principles of Good Governance are upheld for effective Public Resource Management and predictable social services, sustainable growth, economic diversification, social security and inclusive Governance.

4.2 Oversight bodies such as the Parliament, Local Government Councils, the National Audit Office of Tanzania (NAOT), the Commission for Human Rights and Good Governance (CHRAGG), PCCB and boards of various Parastatals should ensure accountability and responsiveness of the executive arm of state for effective public resource management.

4.3 Ministries Departments and Agencies and Local Government Authorities should implement all recommendations by CAG, the Parliament and Local Government Councils to avoid repeated audit queries.

4.4 Appointing authorities should ensure that governing boards of various Parastatals and agencies are timely appointed and oriented on principles of corporate governance.

4.5 The Government should reconsider the ratio of recurrent expenditure to development projects expenditure by significantly increasing the ratio of development project expenditure to recurrent expenditure with emphasis placed on the development of basic infrastructure and services such health, education, food and water.

4.6 Revenue collection should be done in a more customer friendly manner. The use of threats and coercion by Government officials rather than positive motivation is not a sustainable approach as the citizens remain out of sync with Government resource mobilization efforts.

4.7 Scale up implementation of Transparency Enhancing Elements (including giving public the right to review contracts). Transparency is a cornerstone of good governance and is vital in combating corruption in terms of how much companies are paying to government as taxes and royalties.

4.8 NAOT needs to establish online auditing scheme for auditing our foreign embassies. This will help overcoming the travel restrictions due to COVID 19 pandemic.