Dar es Salaam. Have you ever thought that some of your financial problems could be solved in just a matter of few minutes, in the palms of your hands?

The rise of fintech operators is changing the way of accessing quick loans in the age of widespread usage of mobile communication gadgets especially tablets and smartphones.

Telecoms operators started with simplifying the transfer of money through their mobile money wallets and later these systems were integrated with banking services for depositing and withdrawals.

Today, one can transfer, deposit, save money and even quickly borrow in the comfort of his or her home, thanks to the digital ways adopted by the telecoms, banks and other microfinance institutions.

While mobile money services like M-Pesa, Airtel Money, Tigo-Pesa and Ezy-Pesa are designing quick loans for their customers, other firms including Tala and Branch are even stirring up the trend.

Mr Martin David is one of the users of digital services to secure quick loans.

“Can you imagine, in just a matter of few minutes I can get Sh20,000 when I’m low of money for food. I can just borrow and instantly get it,” he said.

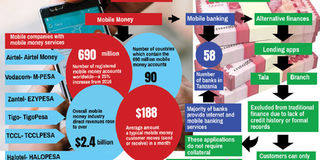

Alternative finances

Lending apps like Tala and Branch have come out to reach customers who have been excluded from traditional finance due to lack of credit history or formal records. These companies offer a loan starting from Sh3,000 to Sh1 million.

They use data like communication patterns, merchant transactions, app usage, and personal identifiers for the purpose of understanding a user’s potential financial capacity, their behavioral attributes, and to validate their identity.

Unlike the traditional banking system, these applications do not require collateral and customers can only borrow again once they’ve paid back.

For others, these apps can offer them confidentiality in borrowing.

“Who’d like to be seen on a bank queue where your whole reputation is at risk,” stated Mr Rajabu Temu, a shopkeeper, who has experience in borrowing through these mobile apps.

“I always borrow through these apps and it’s helping to grow my business,” he said.

Tala operates in Kenya, Tanzania, the Philippines, and Mexico, and has launched a pilot in India. The company has delivered more than $500 million in credit to millions of customers.

It has more than 300 employees in Santa Monica, Nairobi, Dar es Salaam, Manila, Mexico City and Bangalore.

In April this year, the fintech company announced to have raised $65 million in Series C equity investment and debt financing to fund its newly launched global expansion.

Recently, the company announced a strategic investment from global credit PayPal.

On the other hand, Branch, which operates in Kenya, Tanzania, India, Mexico and Nigeria, is expected to have over one million users. It processed six million loans and disbursed about $250 million loans so far across countries of operations.

Analysts say the rapid growth in smartphone use across the developing world has enabled companies like Tala and Branch to flourish.

Findings from FinScope 2017 survey indicate that one of the main drivers of access to financial services in Tanzania has been the take-up of digital financial services which require mobile phone ownership, a registered mobile money wallet or access through a third-party.

It was also found in the study that 63 per cent of adult Tanzanians own a phone, while four per cent (adults from poor households, people living in rural areas, young people and farmers) have a SIM card which they insert in other peoples’ phones.

It’s estimated that only 17 per cent of adults have access to banking services in Tanzania.

M-Pawa - a banking product held by CBA Bank that allows Vodacom’s M-Pesa customers to save and borrow money through mobile phone while also earning interest on money saved – is one of the digital platforms that is said to reach remote people who have no access to formal banking.

A recent research conducted by the Washington DC-based think tank Centre for Global Development in Tanzania and Indonesia found a large and unexplored demand for mobile saving platforms.

“There is a large potential for mobile savings platforms which commercial banks need to design products that focuses on women. The lenders should now consider women as important and trusted customers. In fact, reaching more rural women helps even the government to cover more people with financial services,” said the centre’s senior fellow Mayra Buvinic, who conducted the research in Tanzania.

“Mobile savings reduce transaction cost, provide privacy and increase economic self-reliance for women who are good at saving.”

These digital loans are considered convenient and in some cases cheaper than the bank loans.

“I have never borrowed but I’m thinking of doing it through digital channels because it’s fast and I don’t need to have a security to acquire it,” said Mr Jacob Mogesi, a Dar es Salaam resident.

Tanzania is now moving to regulate the microfinance business where all providers will be required to be licensed and supervised by the Bank of Tanzania or any other delegated authority.